In October 2012 Social Finance was awarded two Social Impact Bond (SIB) contracts from the Department of Work and Pensions Innovation Fund. Today we are publishing a report looking at the first year of operations for the Energise and Teens and Toddlers SIBs.

One of our most popular reports to date has been the Peterborough One Year On document, published in November 2011 and sharing our learnings from the first year of the Peterborough SIB. At a time where there is an enormous amount of interest in SIBs, but relatively few live examples, the opportunity to learn from them becomes all the more important and we hope this new report will be a valuable contribution to the existing literature.

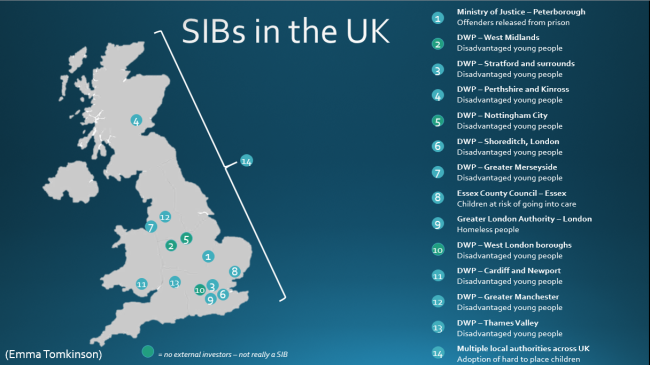

For a more detailed look at where SIBs are active in the UK and internationally, check out this blog from Emma Tomkinson

The SIBs outlined in this report came from a DWP initiative to intervene with young people at the age of 14 with the objective of preventing them from becoming NEET (not in education, employment or training) at 18. The DWP have traditionally intervened with young people who are NEET once they reach the age of 18, but the Innovation Fund contracts see a shift in this focus.

The DWP has identified a number of outcomes against which the contracts will be measured including improved behaviour, school attendance, educational qualifications and employment opportunities. Outcomes payments from the Innovation Fund will be paid over three and half years. Unlike typical social service delivery, the funding is provided at risk by social investors, including Bridges Ventures, Big Society Capital, Barrow Cadbury Trust and the Impetus Trust, whose financial return is aligned to the positive social impact of meeting preagreed educational, training and employment outcomes.

Energise Social Impact Bond: The Energise programme offers mentoring combined with structured activity days and residential courses designed to foster re-engagement with school, to build self-esteem and to improve interpersonal skills. Energise is delivered by the Adviza Partnership and the programme is managed by Social Finance. The programme combines bespoke and generic activities to address individual needs. It is aimed at supporting more than 1,500 young people aged 14 to 16 who are at risk of becoming NEET over a three and a half year period.

Teens & Toddlers Social Impact Bond: The Teens and Toddlers programme combines an 18-week intensive intervention with regular support through to GCSEs. The programme is unique because it targets two sets of vulnerable children simultaneously, raising the aspirations of young people from disadvantaged areas by pairing them as a mentor and role model to a child in a nursery who is in need of extra support. It aims to support more than 1,150 young people aged 14 to 16 who are at risk of becoming NEET over a three and a half year period.

What have we learnt?

Both projects required a bespoke case management system to track each individual at every stage of their personal journey, and to ensure that they are accessing the appropriate level of support. A common theme across both projects has been the time this has taken to set up, as well as the time required for staff to adapt to a new, perhaps more extensive data capturing system than they were used to.

Within the first few months we had data that led us to adapt the Energise programme. We saw that the residential course wasn’t having the desired impact and would have further value if it ran for longer, and was more intensive.

We have also used data to inform adaptations to the Teens and Toddlers delivery model. A decision was made to provide support through to GCSE’s, whereas previously the programme had ended before this milestone. When attendance on this part of the programme began to decline, the intervention was changed to reflect better the needs and interests of young people. The programme now includes activity days and tutoring support in addition to the core service provision.

The Innovation Fund is testing the following hypothesis – if you identify a vulnerable cohort, and invest in prevention, can you reap the social and financial rewards of diverting this group from requiring acute services? The principles behind this span social issues; diverting ex-offenders from returning to crime, diverting children from entering care, diverting emergency hospital admissions – at a time of budget constraints, the case for investing in prevention is stronger than ever.

Social Finance is working to develop Social Impact Bonds across a range of social issues. For those working in areas with a consistent lack of investment in prevention, SIB funding may allow for innovation to be tested, with the risk transferred to social investors. There is £60 million in outcomes funding available in Outcomes Funds administered by the Big Lottery Fund and Cabinet Office, as well as up to £3 million in development grants to refine a SIB proposal. We are working in partnership with the LGA to deliver a support contract on behalf of the Big Lottery Fund, to encourage applications to the Funds. More information about the support available can be found here.

We hope projects like the two listed above will encourage more commissioners to look into the SIB mechanism and the potential it has to transform services in areas affecting the most vulnerable in our communities.

By Sarah Henderson, Service Manager at Social Finance